How Many Types of Cash Books

Introduction

There are four types of cash books: single-column, double-column, triple-column, and petty cash books. For most people, a cash book is a record with a balance sheet and cash flow statement that is used in accounting. It can also refer to the earlier collection of money on a whim to buy something later, using a coin purse. On that note, the second meaning of "cash book" came to be in reference to the financial statements that most lenders collect to determine if borrowers are creditworthy.

In a cash ledger, these statements would be recorded by the bank: initial deposit, cash is withdrawn, total instalments with interest and total payoffs. In the credit market, all transactions between customers are recorded in a cash ledger by the lender. A cash book contains columns on which entries are made for the following purposes:

Day-to-day cash records,

Day-to-day business notes and transactions,

Year-to-date totals

Income and expenses.

Each page of the cash book starts with columns for the date, type of record, customer or employee, amount, and a summing column. Cash book records may be entered either by hand or by a computer.

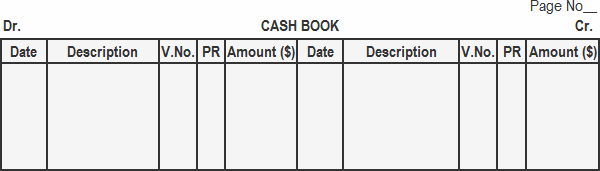

1. Single-Column Cash Book

A single-column cash book is a type of cash book that contains only a single column of transactions. A cash book may contain multiple columns of transactions and/or one or more lines of basic entries. A single-column cash book can be used to record cash transactions such as cash sales, cash purchases, cash trading and banking transactions. It is easier to find transactions in the one-column cash book.

Format of a Single-Column Cash Book

The standard format of a single-column cash book is shown below.

Confused between CGPA and Percentage?

Get your results instantly with our calculator!

Functions of the columns

Date

Cashbook illustrates the history of the business and customers, including where the breakdown of payments took place through dates. The year, month, and day of the receipts and payments of cash are written in the date column on the debit and credit sides of the cash book

Description

The description column contains the company name, the net amount of sales recorded, the merchant’s name, the last date the article was sold, the time the article was sold, and the amount of the sale.

Voucher Number

Voucher number records are usually the result of the efforts of a ledger entry clerk. A ledger that records payments should have voucher numbers at the bottom of each column. This is true also for debits that are used in the payments ledger. These voucher numbers are generally placed on the payment voucher form. This is important so that the ledger clerk, and the invoices clerk who uses the payment vouchers for input, do not have to run all the way down the payments ledger and down through the column where the invoices are supposed to be. If a payment voucher number is removed from the form, unrecorded payments could result.

Posting Reference

A posting reference is used to link a base amount to a transaction that has taken place. When recording a transaction you can use a posting reference to translate the value of the transaction into a number of physical cash items.

Amount Column

The amount column is used to enter the amount received or paid as a result of a cash transaction.

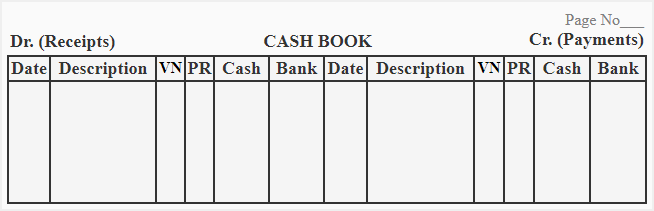

2. Double-Column Cash Book

It consists of two parallel columns of accounts, one for cash and one for bank transactions. Simply by adding a bank column to both sides of a single-column cash book, it is turned into a double-column (or two-column) cash book.

The entries in these columns can only be made in parallel, and the columns must balance. So, this type of cash book is mainly used to track the work, word and labour as well as record the cash paid for purchases for all office supplies, wages of employees and other expenses.

Format of a Double-Column Cash Book

The format of a double-column cash book is similar to a single-column cash book. The exception is that an additional column is included on both sides to record bank transactions.

Cash transactions in a Double-column cash book are recorded in the cash column on the debit side and all cash payments are recorded in the cash column on the credit side. If cash is received from a customer and is deposited into the bank account on the same date, the entry will be made in the bank column on the debit side, not in the cash column.

While doing bank transactions, the following should be considered

The amount of the cheque should be put in the bank column on the debit side when it is received and deposited on the same date into the bank account.

The amount of a cheque should be put in the cash column rather than the bank column when it is received but not deposited into the bank on the same date.

When a cheque from a receivable is deposited into a bank account on a date after it is received, an entry is created in the bank column on the debit side and the cash column on the credit side. It is referred to as a counter entry.

The amount of a cheque is entered only when it is written.

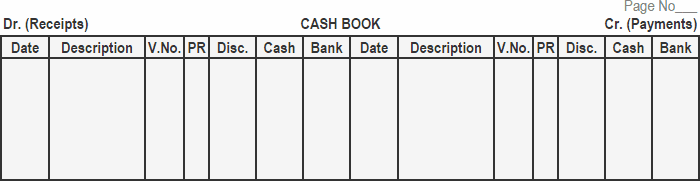

3. Triple-Column Cash Book

Triple-column cash book contains three money columns on both the debit and credit sides: one on each side for recording cash, bank and discount amounts. It's an easy-to-use accounting and record-keeping tool for small businesses. Three sections let one keep all of income, expenses, and cash on hand in a neat, easy-to-see format.

Format of a Triple-Column Cash Book

What to consider while recording discount transactions

On the debit side is the discount received in the column, while on the credit side is the discount allowed column.

The discount columns are essentially memo columns. As a result, the ledger is established with two distinct accounts, "Discount Allowed" and "Discount Received.

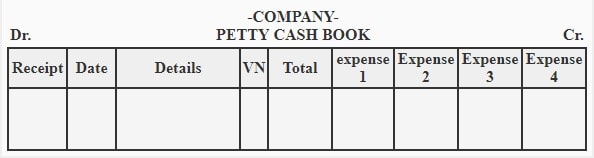

4. Petty Cash Book

As the name implies, a petty cash book is used in an organisation for very small transactions. Such transactions are repetitive and frequently occur, which can place an excessive burden on the general cash book. It is kept in a separate location because of this. Stationery, postage, food bills, fuel, newspapers, and others are examples of such transactions.

Format of a Petty Cash Book

Petty cash systems

The cash allotted for petty expenses for a certain period is written on the credit side of the general cash book and on the debit side of the petty cash book.

The cash is given to the petty cashier whether on the ordinary system or imprest system which is briefly discussed below:

1. Ordinary system: The petty cashier receives a flat sum of money under the standard system. When the entire money has been spent, the petty cashier presents the head or chief cashier with the specifics of the small purchases listed in the petty cash book for inspection.

2. Imprest system: Under the imprest system, the petty cashier is given a specific sum of money known as a float to cover miscellaneous expenses for an agreed-upon period, which is typically a week or month. The chief cashier receives information about all of the petty cashier's expenses at the conclusion of the predetermined time period. The complete amount of money the petty cashier spent throughout the period is returned to him, and the amount of money he will have ready to spend when the next period begins is equal to the initial amount (i.e., float). The agreed-upon float is always equal to the sum of the petty cash balance and all outlays that haven't been paid back to the petty cashier.

Conclusion

Cash books are accounting books used to keep track of all monetary transactions that are entered into an account. The data entered into cash books varies depending on the industry, but in general, it includes who is involved in the transaction and what the object of that transaction is, such as merchandise or services